As most people know, if you invest in an RRSP in Canada, you are making a deal with the government. The deal is that you take money that you have earned this year and you put it into a registered account, promising that you are going to save it to use when you retire. When it comes to the taxation of this money, the deal is that you get the money that you paid in taxes back this year, and you agree that you will pay tax when you withdraw money from the account in the future.

When an employer sets up a group retirement plan, one of the most significant advantages to their employees is that by saving via payroll deduction into an RRSP, the amount of tax you pay is adjusted at the source. You make group retirement RRSP contributions based on your gross income.

What if you don’t have a group plan as an option? Most people have typically made RRSP contributions from their net, after-tax income. Don’t get me wrong; saving for the future is a great idea, and everyone should have a financial plan that includes retirement plans. But is there a better way to save? Many taxpayers are unaware of the fact that there is an option to allow you as an individual to have your company take your RRSP contributions into account when the amount of tax being withheld at the source is calculated.

Let’s take a look at the T1213, a form you can complete to adjust the amount of taxes you have withheld and how it can make a difference in your daily life while supporting your retirement plan.

In This Article:

- Why is saving for retirement important?

- A Case Study on Saving for the Future

- What is the Advantage of pre-tax RRSP contributions?

- Enter the T1213

- Case Study Continued

- Supercharge your RRSP Contributions Conclusion

Why is saving for retirement important?

In 2024, the RRSP contribution limit is 18% of your earned income, up to a maximum of $31,560. The 18% has always been an interesting number to me. If you look at the career path many people currently have, you see a pattern where they work in higher-income earning years for about a third of their lives. So, during these years, you can save up to 18% of your income, and then the idea is you will use those savings to support yourself during retirement. Where the numbers get interesting for me is that as life expectancy has increased and people try to retire earlier, it isn’t unusual to see people end up in a situation where they are retired for about a third of their life as well. So that 18% you were allowed to save, plus its growth, now needs to support you for the same amount of years you were putting money away for. Do you want to reduce your lifestyle in retirement? Probably not, so anything you can do to make your savings work faster for you, the better off you are in the long run.

A Case Study on Saving for the Future

Let’s look at an example to see how RRSP contributions can be amped up. Our test subject is a taxpayer who lives in Ontario and earns $125,000 annually as a T4 employee at a company. The maximum that this person could apply to their RRSP is $22,500 (18% of their income). This equates to $1,875 each month. In Ontario, after taxes, you net $93,475 after taxes on a salary of $125,000. This is $7,790 a month net income.

Now, let’s set the scenario up. Your goal is to max out contributions for this year as well as to begin to use up some of the $100,000 in the back RRSP room that you have built up. To do this, your goal is to set aside $2,000 a month for your RRSP. If you do this from your current net earnings, you have $5,790 to live on each month. This may sound like a lot of money, but if you remember that rent or mortgage payments and utilities will likely eat up at least $3,500 a month, transportation costs make up another $1,000, and other miscellaneous expenses (like food and clothing) can quickly make it so that you realize if you do contribute the $2,000 a month you won’t have the cash flow to support your life.

What is the Advantage of pre-tax RRSP contributions? (a side note for our case study)

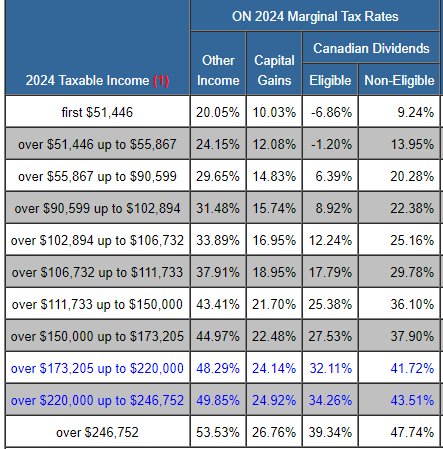

You need to truly understand how Canada’s marginal tax system works to understand what we are talking about fully. You’ve probably heard people talk about tax brackets in the past, but do you know what it means? In Canada, the amount of tax you pay on your income is different based on how much you earn. The more you make, the more tax you pay on the next dollar of income you have. Continuing with the example, if you earned $125,000, the marginal tax rate in Ontario is 43.41%. This means that if you earn $125,001, you pay 43.41% income tax on that extra dollar. It doesn’t mean that you’ve paid 43.41% tax on all of your income, though. In fact, if you calculate the average tax rate for someone who makes $100,000 in Ontario in 2024, their average tax rate is 25.22%.

Here is a table that shows the combined federal and provincial marginal tax rates for Ontario that helps explain how the system works. Note that T4 income would fall into the ‘Other Income’ column.

This chart was sourced from: https://www.taxtips.ca/taxrates/on.htm *Copyright © 2002-2024 Boat Harbour Investments Ltd.

Now, if you look at an RRSP contribution from after-tax income, how it works is that you deduct the amount you contribute from your income and receive a tax refund for that money. So, rolling on with the $125,000 example, if you put $5,000 into your RRSP, you reduce your income to $120,000 and receive a tax refund of $2,170. Sounds pretty good, right? You need to remember, though, that to contribute $5,000 from your net income, you need to earn $7,200 (roughly). This is because, with source tax deductions, you need to earn more to have that $5,000 to put into your RRSP. It’s a vicious cycle where, in order to put away more of your net income, you pay more tax, so you have to earn more to save the same amount. To quote from the old overnight infomercials…There’s got to be a better way!

Enter the T1213!

It is time to introduce our secret weapon, no, not the Slap Chop, it’s the T1213 from the Canada Revenue Agency! You can use this form to apply to have the taxes deducted at source reduced based on expected tax deductions for the upcoming year. You will be required to provide proof of ongoing contributions to your RRSP, but when completed, the CRA will review your case and provide you with a letter to take to your employer to adjust your income for the purpose of taxation.

And now, Back to our Case Study!

Continuing with our earlier example, if you are approved using the T1213 to make $24,000 in annual RRSP contributions ($2000 a month), your taxable income is effectively reduced from $125,000 to $101,000. Here’s where some math pops up (sorry, but it does help show why to do this). Earning $125,000 in Ontario nets you $93,475 after tax. This means that you need to deduct $24,000 from that number to make your RRSP contribution. Sure, it generates a $9,552 tax refund for you, but that comes next year. Your available cash flow this year is $69,475. If we use the T1213, we only pay tax on having $101,000 in income. This nets $79,027 for you this year after taxes, and there’s still $24,000 put into savings for your retirement.

Taking advantage of this opportunity makes approximately $9,550 more available to you as take-home pay. That’s magic; if you look back, that amount matches what you would have received in a tax refund after letting the government hold your money for you for a year while they pay you no interest! This is extra cash flow for you every month, allowing you to help fund your current lifestyle. In effect, what filling out the T1213 does for you is that it gets you your tax refund on each and every pay cheque as opposed to waiting for April when you file your taxes. This means you have more cash available to you every week while still being able to save for the future.

Supercharge your RRSP Contributions Conclusion

The T1213 is a powerful tool that not many people know about. You need to understand that it isn’t guaranteed. The Canada Revenue Agency has to approve you for using it, and if you don’t actually make the contributions that you say you were going to, you have now underpaid your taxes and will owe money. It may also get harder to be approved for using the T1213 in the future. How can this help you? We have teams of Experts at Strata Wealth & Risk Management and Strata Accounting that can work with you to create that financial plan and take advantage of strategies to maximize your savings and bring your goals and dreams a bit closer to coming true. Reach out to us today to find out how!