Canadian entrepreneur and philanthropist Seymour Schulich holds a unique place in the financial landscape of the country. Known for his successes in the mining sector, Schulich is also notable for his philanthropic activities. But there’s another distinction to his name: he’s reported to hold the largest Registered Retirement Savings Plan (RRSP) in Canadian history, with an estimated value in excess of $250 million. Mr. Schulich doesn’t talk about this publicly, but that amount of money has significant tax implications as it comes out of the registered environment.

First, let’s make sure we are all on the same page when talking about the RRSP in Canada. An RRSP is not a product. You cannot ‘buy an RRSP’ to help with your tax planning. An RRSP is a tax-advantaged account designed to help Canadians save for retirement. Contributions to an RRSP are tax-deductible, and investments within the account grow tax-free until withdrawal. As a simplified concept, think of your RRSP as a box that holds investments. You put money that you earned this year into the box. The deal is that you won’t take any money out of the box until you retire. The government gives you back the income tax that you paid on whatever goes into the box the year you deposit it there. You don’t pay taxes as the investments inside the box grow, but when money is taken out of the box, you will pay tax on it then. The reason that it works well for many Canadians is that they will pay a lower tax rate in retirement than they pay while they are working, so there are tax savings associated with this.

On the surface, an RRSP of $250 million is a remarkable achievement and a testament to Schulich’s financial acumen. However, it also carries significant tax implications upon the owner’s death, which can often be overlooked. Upon the owner’s death, there is what is called a deemed disposition. This means that for the purpose of your estate, the government views it as if you sold everything that you owned right before you died. When an RRSP owner dies, their estate will have to pay taxes on their registered savings. The one way that taxes can be deferred further is that registered savings can be rolled on a tax-deferred basis to your partner (common law or spouse). This is only a deferral, though; when the surviving spouse passes away, another deemed disposition happens, and taxes are paid. Inevitably many people have heard the saying that the only things in life that are certain are ‘death and taxes.’ Like many well-known quotes, the reason they are famous is because of how true they are. Everyone dies, and everyone pays taxes. When you die can’t be controlled, but the amount of tax you pay can be helped with some sound financial planning.

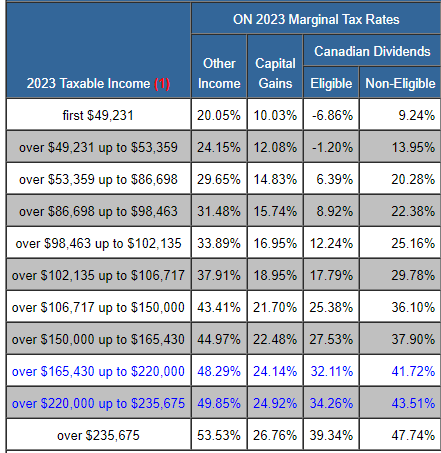

Understanding how income tax is calculated in Canada is important when you look at estate planning for taxes on registered investments. Canada works on a system of tax brackets. What this means is that every dollar that you earn is not taxed equally. The more income you have, the higher amount of tax you pay. This can be a confusing concept, so here’s a table that shows the ‘brackets’ illustrating the tax rates for 2023’s federal and provincial taxes for someone who lives in Ontario.

(Source:https://www.taxtips.ca/taxrates/on.htm)

To try and understand what this means, we can look at an example. If you made $52,000 in taxable income, you would pay 20.05% tax on the first $49,231 and then 24.15% on the $2,769 that falls into the second bracket. When someone talks about a marginal tax bracket, they are referring to what you would pay on the next dollar that you earn. In the example of someone making $52,000, their marginal tax rate is 24.15% because that is how much tax you would pay on the next dollar you earn. Consider now the idea of the deemed disposition we mentioned earlier when that taxpayer is the owner of a $250 Million RRSP; when they die and need to report all the income at once, you can see that they are well into the highest bracket of 53.53% for every dollar over $235,675. In fact, if you apply this combined tax rate to Schulich’s estimated RRSP value, his estate would face a tax bill of approximately $133,242,000. The tax rate on this would be 53.53%. You can see it is slightly below 53.53% total, that is because the estate would owe less than that amount on the first $235,675, but since the amount is so much higher than this, the overwhelming majority of the money is taxed at 53.53%. This would likely be one of the largest tax payments associated with an RRSP in Canadian history.

As mentioned earlier, the taxes on registered savings plans can be deferred as long as the account is transferred to a spouse/common-law partner. This doesn’t eliminate any of the tax burden, but it does delay it until the second spouse passes away.

Another tax-planning option is to donate the RRSP to a registered charity upon the owner’s death. This would lead to the generation of charitable tax credits that could be claimed on the terminal tax return, offsetting some of the income tax owed by the estate. The limit on these credits is 75% of your net income, so you cannot offset everything that is owed, but it could definitely lighten the tax burden on an estate that owned an RRSP worth $250 Million.

I understand how using the example of a person who owns an RRSP that holds an estimated quarter of a billion dollars is extreme. In fact, it is so much money that it can make things hard to relate to as an individual who has nowhere near that amount. Honestly, if the owner of that RRSP withdrew all of the money as a lump sum and paid the taxes while they were alive, they would be left with approximately $117 Million. This after-tax number remains in the stratosphere where most people would be ecstatic with that amount and happy to live out their days spending that during retirement. I know I would. Here’s what using such an extreme example gets us. It highlights the value of making sure that you plan for your future. One of the main things that your financial advisor should be discussing with you is how to work with your team of tax professionals to minimize the income taxes that you pay now and in the future. Sure, you may not be dealing with hundreds of millions of dollars, but in reality, for someone who isn’t at that level of savings, the idea of tax planning becomes far more important. Knowing how to make tax-effective withdrawals from your registered savings plans is a key portion of any financial plan to prolong your savings and protect your legacy into the future.

At the end of the day, the RRSP is a powerful tool for accumulating wealth; understanding the tax implications upon death is crucial to ensuring the benefits are maximized for future generations or charitable causes. Make sure that you make use of your professional team. Tax advisors, financial planners and insurance advisors can help significantly with putting together a plan to maximize the return from your RRSP. If you would like more information on RRSP contributions and tax saving strategies reach out to one of our financial advisors today.